The geography buyers think they are buying is wrong. "Seattle 3PL" almost never means downtown Seattle. Industrial inventory inside the city is declining via conversion (WareCRE flagged 238,811 SF lost to conversion in the latest cycle), and Seattle Close-In (SODO, Georgetown, Interbay) is only 9.5 percent vacant urban infill at a premium to the suburban workhorse clusters. The real workhorse is the Southend (Kent, Renton, Tukwila, Auburn, Federal Way) at 123.3 million SF of inventory, plus Pierce County (Tacoma, Lakewood, Puyallup, Fife, Sumner) at 100.9 million SF, the value leader on dollars per square foot with direct Port of Tacoma drayage. Port of Tacoma's own FTZ #86 page describes Kent Valley as "the second-largest concentration of warehouse and distribution centers on the U.S. West Coast." A buyer who signs an inside-Seattle lease is paying a 25 to 40 percent premium for last-mile geography most brands do not need. The Reddit consensus is uniform: most of the startup-friendly warehouses got priced out to Spokane or Boise, and the boutiques that remain in Seattle proper are either massive (Geodis, DCL) or niche specialists.

NWSA (the Northwest Seaport Alliance combining Seattle and Tacoma) handled 3,156,598 TEUs in 2025, down 5.5 percent year over year, with full international imports falling 10.3 percent to 1.16 million TEUs, the steepest drop of any top-10 US port (KBC Advisors Year-End 2025). YTD April was +15.9 percent before the April tariff regime reversed the trajectory; December imports finished -25.3 percent. That contraction is exactly why the leverage is real. NWSA still ranks as the 4th-largest North American container gateway, and West Coast labor is stable through July 1, 2028 under the ILWU-PMA Pacific Coast Longshore Agreement ratified August 2023. The East/Gulf ILA-USMX contract by contrast runs only through September 30, 2030 and was won at the cost of a 2024 strike that closed every East/Gulf port for three days. For brands choosing a 2026 fulfillment node, the strike-risk math now favors NWSA over the East Coast for the first time in two decades. SEA (Sea-Tac) handled 427,971 metric tons of air cargo in 2025 as the secondary lane for high-value or time-critical Asia imports. FTZ #5 (King County) hosts Tommy Bahama, Juno Therapeutics, and Honeywell Aerospace (approved August 15, 2025); FTZ #86 (Pierce County) is the 4th-largest FTZ on the US West Coast by merchandise received and overlaps the Kent Valley directly.

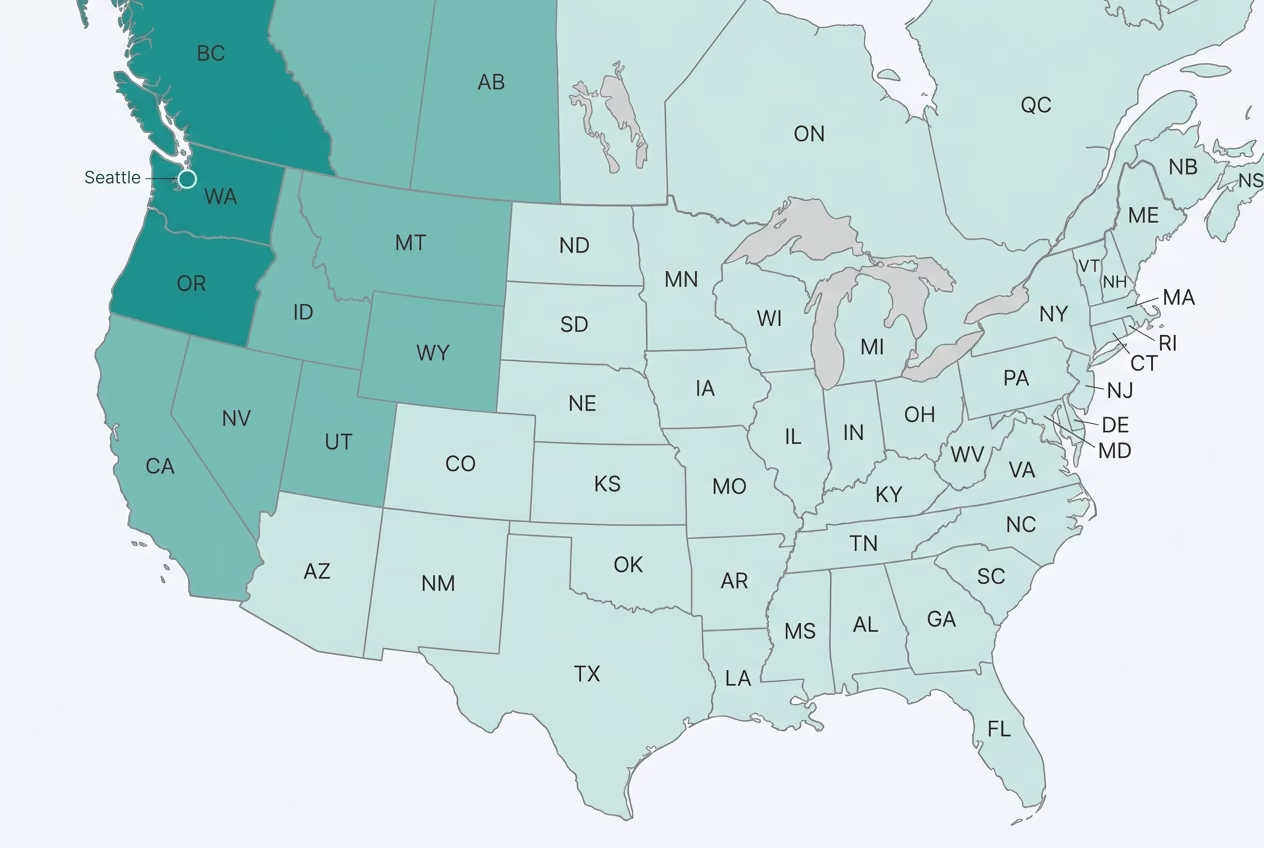

Section 321 de minimis was fully suspended on August 29, 2025 per Executive Order. For a decade, Canadian 3PLs in Surrey and Richmond BC injected sub-$800 parcels into the US last-mile via Blaine, WA duty-free. That model is dead. Vancouver BC sits 141 miles north of Seattle, about 2 hours 40 minutes by truck. The defensible 2026 move for a brand previously running Vancouver BC for US fulfillment is a Kent or Fife facility plus a cross-dock back into Canada Post when needed, same continental position, no per-parcel cross-border duty hit, and the FTZ #5 or FTZ #86 weekly-entry program absorbs the new tariff overhead. Per GoBolt's February 2026 brand survey, 22.5 percent of cross-border brands are shifting inventory to US and Canadian warehouses for domestic fulfillment post-321. Drive times from Seattle: Portland 3 hours, Spokane 4 hours 34 minutes, Vancouver BC 2 hours 40 minutes, Salt Lake City 12 hours 18 minutes. That geographic position, anchored by Amazon (multiple Kent FCs including BFI4 at 21005 64th Ave S), Microsoft, Costco, Starbucks, Nordstrom, and Boeing (Everett 777/767/737 MAX 10 fourth line, Renton 737 final assembly, Auburn fabrication), is the foundation for how we route inbound and outbound.